Heath Goldfields announced its first gold pour on 19 February 2026, marking the restart of a mine that had lain idle for two years. The company said about 1,400 workers had returned to payroll as operations resumed at Bogoso-Prestea.

Within weeks, the project was further boosted by a Trafigura offtake agreement covering 700,000 ounces of gold doré, alongside $65 million in debt financing. The development quickly drew international attention, with Bloomberg reporting on what appeared to be a fresh chapter for Ghana’s mining sector.

On the surface, it is the kind of narrative Ghana’s mining industry has been eager to tell: a locally anchored company reviving a historic asset, attracting global commodity finance, and doing so at a time when gold prices have surged past $5,000 an ounce—one of the sharpest rallies since the late 1970s.

As Africa’s largest gold producer, Ghana has leaned into a renewed sense of confidence in its mining sector. There is a growing belief that the country can take greater control of its mineral wealth while riding a powerful global commodities cycle.

But beneath the headline milestones, the Heath Goldfields story tells a more complicated tale. Stripped of the surface optimism, it becomes a case study in how resource-rich countries can still struggle to convert geological endowment into lasting industrial success, even during historic commodity booms.

At the centre of it all is Bogoso-Prestea, a mine that has produced more than nine million ounces of gold since 1912. Yet, despite that extraordinary output, it remains in 2026 a symbol of repeated cycles of investment, decline, and reinvention.

Over the decades, nearly every operator that has taken control of the asset has either exited under financial strain or been removed amid operational or regulatory disputes. That history raises broader questions that continue to shadow Ghana’s mining industry: why has it been so difficult to build a long-term, globally competitive mining champion? Why do flagship assets like Obuasi and Bogoso-Prestea not reflect the scale of their geological wealth? And why does sustained value creation remain elusive despite decades of extraction?

Nine Million Ounces and Counting

Bogoso-Prestea lies along the southern edge of Ghana’s Ashanti Greenstone Belt, a 250-kilometre stretch of Paleoproterozoic rock widely regarded as one of the world’s richest gold-bearing formations. The belt also hosts major mines such as Obuasi, Tarkwa, Wassa, and Damang.

Mining activity at Prestea dates back to at least the 1870s, when early European prospectors first worked the area. By 1912, Ariston Gold Mines had developed more structured underground operations, sinking shafts that still form part of the mine’s core infrastructure today.

Following years of state consolidation and later divestment, output at Bogoso-Prestea declined sharply, falling to just over 20,000 ounces in 1984 under state management—an early sign of the long and uneven operational history that would follow.

When viewed across its full history, the Bogoso-Prestea mining enclave stands out as one of Ghana’s most mineral-rich yet troubled assets.

In the early 1960s, the Government of Ghana acquired several mining interests along the belt and consolidated them into Prestea Goldfields under the State Gold Mining Corporation (SGMC). At its peak in 1964, the operation produced about 167,000 ounces of gold annually, with exceptionally high recovered grades averaging 11.6 grams per tonne. In some underground sections beneath Prestea, particularly along the West Reef, fault-fill quartz veins have returned sample grades exceeding 100 grams per tonne—figures that underscore just how rich the deposit can be.

These are the kinds of numbers that typically attract major global mining houses. A 2017 technical report estimated that as much as 5.1 million ounces of gold may still remain within the Bogoso-Prestea concession. It also projected average underground grades of around 8.1 grams per tonne, with potential metallurgical recoveries of up to 94% using carbon-in-leach processing.

On paper, the site is exceptionally well-endowed. It includes two operational shafts, a 1.5 million-tonne-per-annum carbon-in-leach plant, and a BIOX® sulphide processing circuit. In exploration terms, it resembles the kind of long-life asset junior miners spend decades searching for. In operational reality, however, it has repeatedly proven difficult to sustain.

Since the late 1950s, the mine has passed through multiple hands. It was nationalised after independence and later brought under the State Gold Mining Corporation. Following years of underperformance and structural decline, it was reopened to foreign investment in the 1990s. From there it moved through several operators, including Barnex JCI, Prestea Gold Resources, and eventually Golden Star Resources—a Canadian company once backed by billionaire Naguib Sawiris, which acquired the Bogoso concession in 1999 and the Prestea underground mine in 2001.

Golden Star invested heavily in the asset, refurbishing shafts, upgrading ventilation systems, introducing BIOX® technology, and deploying mechanised mining methods such as Alimak shrinkage stoping. Despite these efforts, the underground operations remained inconsistent. By 2019, the company had written down the mine’s value by $56.8 million and reported annual losses of about $78 million. The challenges were persistent: complex geology, uneven “nuggety” gold distribution in the West Reef, and recurring water ingress at deeper levels.

When Golden Star announced the sale of Bogoso-Prestea to Future Global Resources (FGR) in July 2020 for up to $95 million, it was framed as a fresh start. FGR, a London-based entrant, was expected to bring new capital and renewed focus, while Golden Star shifted attention to its Wassa operations. But the structure of the deal suggested a more cautious reality: only $5 million was paid upfront, with the remainder staggered over several years and partially contingent on future sulphide production.

London Calling, Accra Fumbling

FGR itself was an unusual buyer for a major mining asset. Incorporated in December 2019 under Blue International Holdings, it was led by investors Andrew Cavaghan and Mark Green—figures with finance backgrounds but limited mining experience.

Blue International’s wider portfolio included renewable energy developer Joule Africa, and its advisory board featured high-profile names such as former British Army chief Lord Dannatt, former Foreign Office minister Lord Triesman, and Philip Green, who was attempting to rebuild his reputation following the collapse of Carillion.

A later investigation by The Guardian revealed a complex web of financial and political links. John Glen, a UK Treasury minister between 2018 and 2023, held shares in Blue International. The UK government’s Future Fund also extended £3.3 million in support. Meanwhile, Devonport Capital—an emerging markets lender led by Paul Bailey and Thomas Kingston, a Foreign Office veteran married to Lady Gabriella Windsor—provided around $5 million in financing.

As the Ghanaian operation deteriorated, financial pressure spread through the network. Devonport Capital’s own creditors, including Legatum founder Christopher Chandler and the UK tax authority, were drawn into the fallout. Thomas Kingston died in February 2024, and by the following year Devonport had entered administration with tens of millions in outstanding liabilities and limited recovery prospects.

On the ground in Ghana, FGR’s tenure at Bogoso-Prestea was marked by operational breakdowns, unpaid wages, and rising debts to suppliers and utilities. The Ghana Mineworkers’ Union described surrounding communities as becoming “virtually ghost towns,” while the company also struggled to meet obligations to the state power utility.

Workers staged protests—some accompanied by brass bands—carrying placards that read “Blue Gold is a scam.” Despite this, the asset was later restructured under a new corporate identity, Blue Gold, and listed on NASDAQ via a merger with a special purpose acquisition company. The company announced it had secured about $140 million in restart financing, including $65 million held in escrow, though disbursement remained unclear.

The stock’s performance told its own story: Blue Gold’s share price collapsed by more than 96%, while the company reported no revenue, a $15.1 million annual loss, and a working capital deficit of $10.7 million.

It was against this backdrop that Heath Goldfields emerged in early 2024. The company was incorporated on 6 February 2024 with a stated capital of just GH¢10,000 (about $700). Within a week, it had applied for a mining lease still formally held by FGR/Blue Gold. By September 2024, the Minister for Lands and Natural Resources had terminated the existing lease, and by November the Minerals Commission had approved its reassignment to Heath Goldfields.

Within days of a letter reportedly pausing the transition, Heath personnel were said to have mobilised to the site, asserting control over equipment, accommodation facilities, and gold stockpiles.

Questions soon followed over the company’s true backers. In its initial presentation to the Minerals Commission, Heath Goldfields was described as a subsidiary of Turkey’s Yildirim Group, a major industrial conglomerate whose mining arm, Yilmaden, operates internationally. The proposal was also accompanied by claims of a $500 million investment commitment outlined in its strategic plan.

On the strength of these claims, or more likely the relationships, the award of leases followed.

But it didn’t take long for problems to emerge.

The Catchment Area Community Alliance, a local youth group, later petitioned the government, pointing out that publicly available records on the Yildirim Group’s corporate structure do not show Heath Goldfields as one of its recognised subsidiaries or affiliated entities.

That finding raised fresh concerns, particularly because officials at the Minerals Commission had earlier assured the Minister—in an October 23, 2024 letter—that Heath Goldfields was indeed owned by the Yildirim Group, alongside a range of other supporting claims and commitments.

The much-publicised half-billion-dollar funding package for Heath Goldfields has yet to materialise in full. Despite early assurances, several of the expected financial commitments have not been realised, and none of the Minerals Commission officials who reportedly described Heath as a subsidiary of a Turkish conglomerate have publicly accounted for those claims.

As the anticipated Turkish backing faded, a revised list of financiers began circulating, presenting a very different picture of the venture’s financial foundation:

| Source | Amount |

|---|---|

| Shareholder loan | $30 million |

| Trafigura financing | $65 million |

| ECOWAS Bank for Investment & Development | $100 million |

| First Atlantic Bank | $5 million |

| Guaranty Trust Bank | $6 million |

In the months that followed, however, much of the expected funding pipeline appeared to stall. The recent Trafigura arrangement—combining a gold offtake agreement with $65 million in debt financing—now stands as the only major tranche to have materialised. While significant, it falls far short of the original multi-source pledge once touted for the project.

Changing Financial Architecture and Political Linkages

Recent changes in corporate filings have also brought renewed attention to the domestic political and corporate networks surrounding the venture.

Dr Kwabena Duffuor, former Finance Minister and one of Ghana’s most prominent businessmen, is listed as a director. His son, Dr Kwabena Duffuor Jnr, serves as Board Chairman.

Other early filings name individuals such as Sylvia Naa Odarley Amporful and lawyer Edwin Kpedor, whose name appears across multiple related corporate documents. The entity Eureka Capital—previously linked in other Duffuor-associated commercial disputes—also features in the structure.

Notably, the Turkish investor group initially presented as the venture’s technical and financial anchor has since disappeared from the company narrative.

Workforce Reductions and Labour Disputes

Since Heath Goldfields assumed control, reports indicate that more than 400 workers have been laid off under what the company described as operational restructuring. The dismissed workers have since publicly accused the company of deception, unfair treatment, and failure to meet financial obligations.

According to worker representatives, only partial salary arrears have been paid. Outstanding obligations reportedly include severance packages, provident fund contributions, bonuses, and repatriation entitlements.

Although a GH¢136 million settlement was later announced, questions remain over how much of it has actually been disbursed. Political figures within the ruling party have called for the lease to be terminated and reassigned to a more capable operator, a position echoed by some local traditional authorities. The controversy has intensified scrutiny over whether Heath Goldfields has the technical expertise and financial capacity required to manage one of West Africa’s more complex gold assets.

Trafigura’s Calculated Position

The April 2026 Trafigura offtake agreement has attracted particular attention—not only for its size, but for what it reveals about the financial pressures surrounding Heath Goldfields.

Trafigura, a global commodity trading giant with revenues exceeding $200 billion, has steadily expanded its footprint in African metals markets. Its $65 million financing package is secured against an estimated 700,000 ounces of gold production.

At current prices approaching $5,000 per ounce, the underlying gold stream is worth roughly $3.5 billion. For Trafigura, the exposure is relatively modest within its global portfolio. In return, it secures long-term access to physical gold supply at a time of strong global demand.

For Heath Goldfields, however, the arrangement appears to represent a critical—and possibly only—source of liquidity. Without external funding, even limited restart operations for oxide mining would be difficult to sustain.

The underground mine itself remains severely compromised, with flooding reported well above Level 18. Key infrastructure between Levels 18 and 24, including locomotives, power systems, and ore passes, is believed to be submerged.

Restoring the underground section to operational capacity would require hundreds of millions of dollars in capital expenditure—far beyond the scope of the current Trafigura facility, which is more suited to stockpile processing and limited surface operations.

While the deal may provide short-term relief, questions remain about whether it can meaningfully restore full-scale production. Company hopes that the agreement could unlock additional financing from other investors remain uncertain.

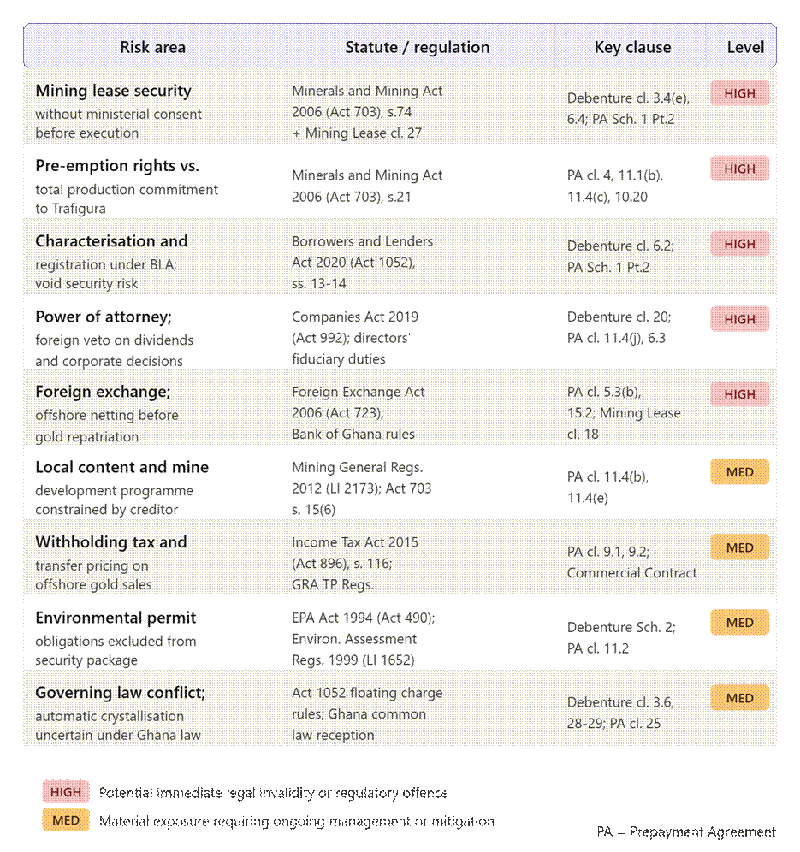

Legal and Regulatory Questions Around the Trafigura Agreement

The structure of the Trafigura-Heath arrangement has also raised legal and regulatory questions, particularly regarding compliance with Ghana’s mining laws.

Under Clause 3.4(e) of the April 2, 2026 debenture, Heath Goldfields’ three mining leases (APL-M-147, APL-M-148, and APL-M-149) are assigned as first-priority security to Trafigura.

However, the agreement also introduces a conditional structure through the “Consent Date,” which defers full effectiveness of the security until ministerial approval is granted. Heath is given 60 days to obtain this consent.

This raises a potential conflict with Section 14 of Ghana’s Minerals and Mining Act, 2006 (Act 703), which prohibits the creation of any encumbrance over a mining lease without prior ministerial approval. While the agreement is structured to take effect conditionally, legal debate centres on whether execution of such an instrument itself already constitutes a form of prohibited disposition.

Further complexity arises from Section 21 of Act 703, which grants the state pre-emption rights over mineral production. Although Clause 10.20 of the agreement acknowledges this, other provisions effectively require Heath to dedicate at least 200% of its production capacity to Trafigura’s offtake commitments, while restricting additional financing arrangements that could interfere with that obligation.

Local Ownership, External Control

The Trafigura agreements also highlight a broader structural concern in the mining sector: the gap between local ownership and actual operational control.

Clause 11.4 of the prepayment agreement grants Trafigura extensive veto rights over key corporate and operational decisions, including dividends, capital expenditure, restructuring, debt issuance, and changes in control.

In effect, while Heath Goldfields operates as a Ghanaian entity on paper, significant financial and operational authority rests with the foreign financier.

A separate share charge further pledges equity held by Eureka Capital to Trafigura. Should enforcement occur, Trafigura could assume effective control of a company holding three active mining leases.

Ordinarily, such a change in ownership would require ministerial approval under Act 703. However, the agreement leaves ambiguity over what happens if such consent is not granted. It also raises unresolved questions about compliance with Ghana’s foreign exchange regulations, particularly in relation to offshore netting of gold proceeds against debt obligations.

A Deal That Reflects a Broader Reality

Taken together, the funding shortfalls, shifting investor narratives, and tightly structured financing arrangements point to a broader reality: control in resource projects does not always align with formal ownership.

In Heath Goldfields’ case, a local corporate structure fronts a project that is increasingly shaped by external financial and operational constraints.

Whether the arrangement stabilises production or deepens existing tensions will depend not only on financing flows, but also on how regulatory and legal questions are ultimately resolved.

Blue Gold Fumes in the Background

Blue Gold’s international arbitration case under the UK–Ghana bilateral investment treaty continues at the Permanent Court of Arbitration in The Hague, where the company is seeking damages estimated at over $1 billion. The stakes are high: if Blue Gold succeeds, Ghana could face severe financial exposure, potentially exceeding the lifetime value of the mine under Heath Goldfields’ current stewardship. If it fails, observers warn the precedent may still deter future foreign investment—particularly given the optics of a NASDAQ-listed company losing its asset, only for it to be handed to a newly incorporated operator with minimal capital.

A Pattern of “Jurisdictional Chaos”

The dispute over Bogoso-Prestea is widely seen as part of a deeper structural problem in Ghana’s mining sector: what can be described as chronic jurisdictional instability. Similar patterns across several African resource economies show a recurring misalignment between regulation, political incentives, and commercial mining realities.

At Bogoso-Prestea, successive operators—from Golden Star to FGR to Heath Goldfields—have operated in an environment where rules appear fluid, tenure feels insecure despite legal documentation, and the state shifts roles between regulator, landlord, partner, and political negotiator.

The same issues were evident at Damang, where a short tender window was created for a mine requiring hundreds of millions of dollars in investment, along with detailed feasibility studies and regulatory approvals. In practice, processes in both cases were so compressed that only well-connected insiders could realistically participate, undermining standard investment requirements and technical due diligence.

Resource Nationalism or Institutional Erosion?

Some view these interventions as resource nationalism. However, critics argue that genuine resource nationalism—such as the structured models seen in Chile or Botswana—depends on strong, predictable institutions rather than ad hoc decision-making.

In those countries, state-owned or national champion models were built on clear rules, stable governance, and disciplined investment frameworks. The argument goes that Ghana appears to be moving in the opposite direction: weakening institutional predictability while attempting to promote domestic control.

The result, critics say, is not strong national champions but a cycle of undercapitalised operators, stalled projects, legal disputes, and abandoned or flooded mining infrastructure.

Lessons from Abroad

International comparisons are often drawn to illustrate alternative approaches. China’s industrial policy, for example, began not with expropriation but with the construction of predictable industrial zones, long-term tax incentives, and massive investment in technical education. Domestic firms were nurtured over decades within stable frameworks before becoming globally competitive.

Similar sequencing is cited in the development paths of companies like Huawei, or national champions in South Korea and elsewhere. The common thread, analysts argue, is institutional stability first—industrial ambition second.

Bogoso-Prestea’s Structural Challenge

Beyond policy debates, Bogoso-Prestea faces severe technical and geological constraints. While the site is rich in gold, much of the remaining resource is locked in deep, water-prone underground sulphide ore requiring capital-intensive processing technology.

Earlier attempts to process refractory ore through the BIOX plant eventually struggled with cost and efficiency issues. Underground flooding has also been a recurring challenge, with repeated cycles of dewatering and re-flooding undermining operational stability.

The scale of remaining resources is still significant, but the technical threshold for extraction is high. Analysts suggest only operators with deep capital reserves, long-term patience, and strong technical capacity are likely to succeed—conditions they say are often absent in the current operating environment.

A Sector Under Pressure Amid High Gold Prices

The instability is particularly striking given favourable global conditions. Gold prices surged sharply in 2025, driven by central bank demand, geopolitical uncertainty, and currency pressures. Industry margins have widened significantly, and African producers are racing to bring new supply online.

Despite this, Ghana’s key assets—including Bogoso-Prestea and Damang—remain tied up in disputes and operational uncertainty. Meanwhile, established large-scale operations continue to dominate production, while smaller-scale operators struggle to transition into more formal, scalable mining enterprises.

Systemic Governance Concerns

At the core of the issue is a perceived gap between political messaging and technical execution. While there is strong public support for greater national ownership of mineral resources, critics argue that policy implementation often lacks the technical sequencing required to translate ambition into sustainable outcomes.

Instead, interventions are frequently described as reactive and politically driven, producing short-term symbolic wins but long-term operational instability.

Operational and Legal Risks Mount

Current conditions at Bogoso-Prestea reflect these tensions. Regulatory concerns have been raised over environmental and safety compliance, including unmanaged underground water accumulation and deficiencies in tailings storage facilities that pose risks to nearby communities.

At the same time, financing arrangements tied to commodity traders and external investors have introduced further complexity, with questions over investment commitments, creditor repayments, and regulatory approvals still unresolved.

There are also indications that planned large-scale investments have not materialised as expected, further complicating the mine’s long-term outlook.

A Call for Structural Reset

Given the scale of the challenges, some analysts argue that a fundamental restructuring may be required. Proposals include creating a special investment vehicle that consolidates existing claims and restructures ownership, potentially allowing current stakeholders to retain minority positions while enabling a new, well-capitalised consortium to take operational control.

The argument is that only a technically strong and financially robust operator, working within a predictable regulatory framework, can realistically unlock the remaining value of the asset.

Broader Lessons for Ghana and Africa

Bogoso-Prestea, with its century-long production history and millions of ounces still in the ground, is increasingly seen as a case study in the gap between resource endowment and governance capacity.

The central lesson, analysts argue, is that resource ownership alone is not enough. Value creation depends on sequencing: building strong institutions, enforcing predictable rules, and then leveraging those systems to attract and discipline capital.

Without that foundation, even high commodity prices and rich deposits may fail to translate into national benefit.

As global attention returns to African gold production, Ghana’s mining sector now sits at a crossroads. The outcome of disputes like Bogoso-Prestea will likely shape not only investor confidence, but also the country’s broader reputation as a stable destination for long-term resource investment.

Blue Gold Fumes in the Background

Meanwhile, Blue Gold’s international arbitration under the UK–Ghana bilateral investment treaty continues at the Permanent Court of Arbitration in The Hague. The company is seeking damages estimated at over $1 billion. If it succeeds, the financial exposure for Ghana could be significant—potentially exceeding the total revenue the mine might generate under Heath’s stewardship.

If Blue Gold loses, however, the precedent could still deter future foreign investment. The optics of a NASDAQ-listed company being stripped of its asset and replaced by a firm incorporated just a week earlier with $800 in capital is not the kind of outcome institutional investors easily forget.

Jurisdictional Chaos as a Structural Problem

The situation at Bogoso-Prestea is not an isolated incident. It reflects deeper, systemic challenges. Ghana’s mining sector—and indeed resource governance across many African countries—often operates in an environment of recurring institutional confusion.

This can fairly be described as chronic jurisdictional instability: a form of what I have previously referred to as “katanomics.” The persistent misalignment between regulation, political incentives, and commercial mining realities is widespread.

At Bogoso-Prestea, every major actor—from Golden Star to FGR to Heath Goldfields—has operated in a system where rules appear flexible depending on political pressure, where tenure security is uncertain despite legal documentation, and where the state shifts roles between regulator, landlord, equity partner, and political negotiator.

A similar pattern was visible at Damang, where a seven-day tender window was opened for a project requiring over $500 million in investment, alongside a bankable feasibility study, environmental assessments, and water-use permits.

In both cases, regulatory timelines were compressed to a point where only insiders could realistically participate. Technical and financial requirements for responsible mining were reshaped by political discretion.

This Is Not Resource Nationalism

It is important to be precise. This is not resource nationalism in the developmental sense.

Successful resource nationalism is what Chile achieved through Codelco or what Botswana built with Debswana. Those models are grounded in institutional discipline, not improvisation. It is not possible to build credible national champions on a foundation of disorder.

Effective national champion development requires first establishing jurisdictional quality—clear rules, consistent enforcement, credible arbitration, and predictable governance. Only then can the state strategically nurture domestic firms capable of competing globally.

What appears to be happening instead is the reverse: a weakening of institutional quality in the hope that national champions will somehow emerge from the resulting instability. The outcome is predictable—under-capitalised operators, recurring disputes, idle assets, and environmental risk accumulation.

Lessons from Global Comparators

China’s industrial development experience is instructive. When building national champions in sectors such as telecoms, semiconductors, and electric vehicles, it did not begin with expropriation or arbitrary asset transfers.

Instead, it built industrial zones with predictable rules, offered tax incentives tied to technology transfer, invested heavily in engineering education, and gradually nurtured domestic firms over decades until they became globally competitive.

Huawei began as a reseller of imported telecom equipment. In South Korea, Samsung started as a trading business. Neither emerged through regulatory shortcuts or administrative fiat.

Similar lessons can be drawn from the UAE’s financial sector development, Chile’s copper governance model, and Indonesia’s nickel downstream strategy. Across all cases, sequencing—not sentiment—was the decisive factor.

The first step is always jurisdictional cleanup: consistent enforcement, credible dispute resolution, and equal treatment of investors. Only then can domestic firms be meaningfully supported without distorting competition or deterring capital.

Ghana’s Inverse Trajectory

Ghana’s current trajectory in the mining sector appears to invert this sequence. Public sentiment strongly favours greater domestic ownership of mineral resources, and political messaging reflects this demand.

However, the technical and institutional capacity required to translate this sentiment into structured policy is often missing.

The result is what might be described as reactive governance: interventions that create the appearance of nationalist action while leaving underlying structural weaknesses intact.

Bogoso-Prestea as a Case Study

Bogoso-Prestea has repeatedly demonstrated the same structural constraints across different operators.

The geology is complex. While initial oxide resources were more accessible, they have largely been depleted. The remaining sulphide ore—estimated at approximately 1.76 million ounces of measured and indicated resources—requires capital-intensive processing technology.

Golden Star Resources previously developed a BIOX® plant to process refractory ore, but it was eventually shut down due to cost and operational challenges. The Prestea underground mine has experienced repeated cycles of flooding and dewatering, reflecting ongoing technical and environmental difficulty.

Sustainable operation at this site requires long-term capital, advanced technical expertise, and regulatory stability. These are precisely the conditions that have been inconsistent.

As a result, operators tend to fall into a pattern: startups, turnaround firms, or politically connected entities rather than established tier-one mining companies. This selection bias is not accidental; it is produced by risk conditions that deter long-term institutional investors.

A Missed Opportunity in a Bull Market

All of this is unfolding during one of the strongest gold cycles in decades. Gold prices rose sharply in 2025, driven by central bank demand, geopolitical instability, and currency weakness.

Industry margins have expanded significantly, with forecasts pointing to sustained profitability for well-capitalised producers. Across Africa, new projects are being fast-tracked to take advantage of favourable pricing conditions.

Ghana, which sits on one of the world’s richest gold belts and remains Africa’s largest producer, should be among the biggest beneficiaries.

Instead, key assets such as Bogoso-Prestea and Damang remain tied up in disputes and operational uncertainty. Meanwhile, large-scale producers such as Tarkwa, Obuasi, and Wassa are likely to remain dominant even as smaller operations struggle to scale.

Structural Lessons for Africa

Bogoso-Prestea is more than a mining case study. It is a reflection of broader governance challenges in resource-dependent economies.

The mine has produced over nine million ounces historically, with an estimated five million ounces still in the ground. In principle, it should be a cornerstone of sovereign wealth creation.

Instead, it is caught between legal disputes, operational uncertainty, and competing claims, while arbitration proceedings involving Blue Gold continue in parallel.

The deeper issue is not any single operator, but a system that prioritises short-term political positioning over long-term institutional continuity.

Between resource ownership and resource value lies the harder task: building credible institutions that govern extraction in a predictable, globally competitive way.

The Situation on the Ground

Current conditions at Bogoso-Prestea remain fragile. Regulatory breaches have been flagged regarding underground water accumulation, while tailings storage infrastructure remains under strain, raising concerns for nearby communities such as Dumasi and Bogoso.

Operational commitments tied to new investments remain uncertain, with questions surrounding financing structures, contractor payments, and long-term capital deployment.

Given these conditions, the situation requires urgent restructuring. One option under discussion is the creation of a special-purpose investment vehicle that consolidates interests, reduces fragmentation, and brings in a technically strong operator through a transparent competitive process.

Under such a framework, existing parties could retain minority stakes while relinquishing operational control, enabling a more credible long-term investor to take over development and management.

Conclusion: The Cost of Institutional Weakness

Bogoso-Prestea contains an estimated five million ounces of remaining gold. Whether that wealth ultimately benefits Ghana or is dissipated through inefficiency and dispute will depend less on global gold prices and more on governance quality.

The central constraint is not geology or capital alone, but institutional design.

So far, the cost of delayed reform continues to accumulate—and the bill for jurisdictional instability remains unpaid.